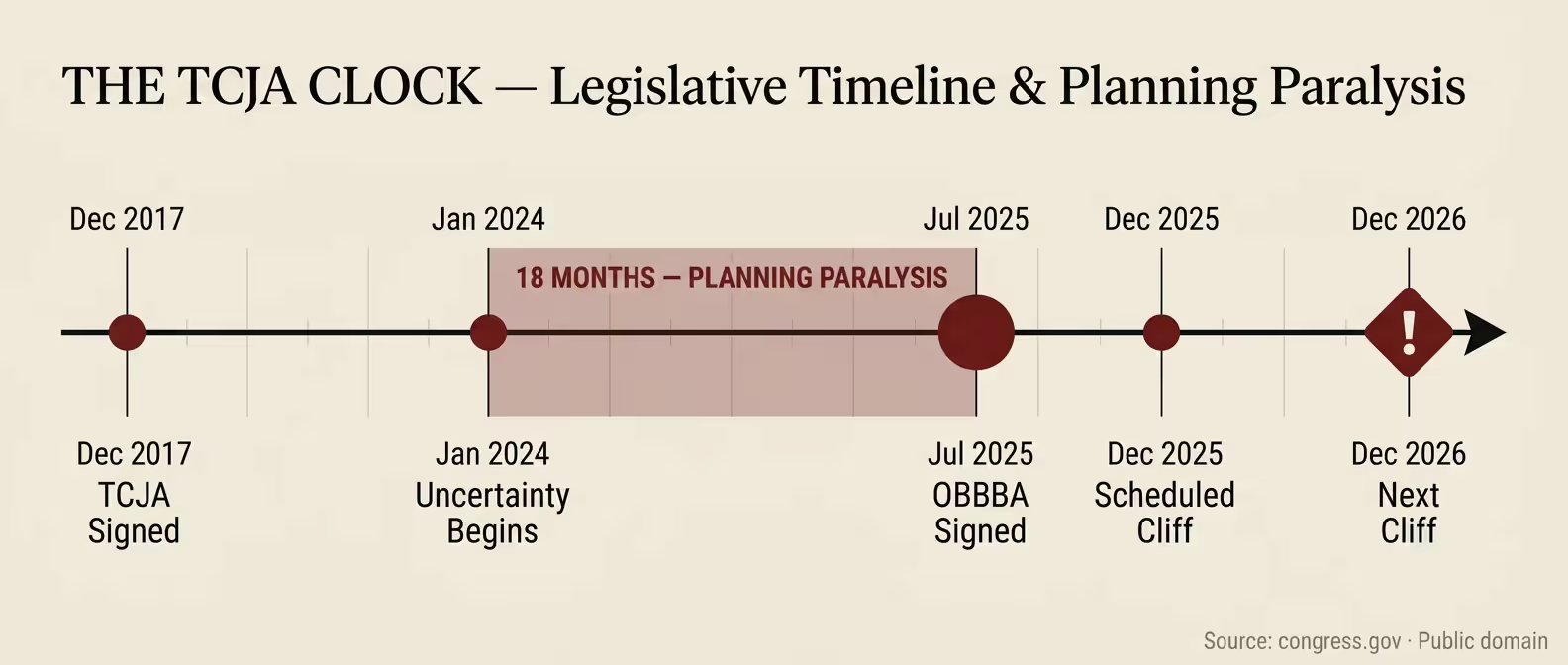

How eighteen months of tax uncertainty paralyzed American business—and what is already scheduled next

A corporation can survive a bad tax rate. What it cannot survive is the blank cell—the line in the financial model that reads: pending congressional action. For eighteen months, American business ran on spreadsheets with blank cells in the tax line. The decisions those spreadsheets could not produce are the gross domestic product that was never reported.

David Morales owns a commercial plumbing and mechanical contracting business in the Chicago suburbs. Thirty-four employees. In January 2024, his accountant told him something that changed how he ran his business: "I cannot build a reliable three-year financial model for you right now. The federal tax rate on your pass-through income is being negotiated in Congress. I do not know how it ends." David put three hiring decisions on hold. He declined a multi-year project that required debt financing—because the debt service model assumed a net cash flow framework he could not confirm. He made the rational decision. When the rules are unknown, the intelligent player waits. Multiply David by 4.6 million pass-through entity owners making the same calculation simultaneously, and you understand what Wall Street meant by shadow volatility.

THE EXPIRATION DATE :The Tax Cuts and Jobs Act (TCJA) of 2017 contained a structural flaw its architects understood and its critics exploited. Most individual and pass-through provisions were written to expire on December 31, 2025—not because they were intended to be temporary, but because making them permanent would have violated the strict Senate budget reconciliation rules that allowed the bill to pass with a simple majority.

procedural artifact became the largest scheduled tax increase in American history. Had Congress failed to act, individual tax rates would have rebounded, the standard deduction would have been slashed from $15,750 back to roughly $9,000 for single filers, and the lifetime estate tax exemption would have cratered from $13.99 million down to approximately $7 million per individual.

Capital expenditure growth in the S&P 500 decelerated sharply from 18.4% in 2023 to 6.2% in 2024— despite robust corporate earnings and record cash balances. Chief Financial Officers cited TCJA sunset uncertainty explicitly in quarterly earnings calls as the primary factor in deferring capital deployment. The shadow volatility that the standard equity volatility indexes failed to capture showed up in physical economic slowdown instead.

THE 199A LIMITATION MOST ADVISORS GET WRONG

While the passage of the One Big Beautiful Bill Act (OBBBA) in July 2025 swept away the cliff by making the Section 199A 20% Qualified Business Income (QBI) deduction permanent, it did not change the math under the hood. Most business owners remain dangerously misinformed about how the deduction actually operates once income moves past specified benchmarks. Above the 2026 inflation-adjusted statutory thresholds—$201,750 for single filers and $403,500 for married filing jointly—the 199A deduction is no longer a simple 20% calculation. For non-Specified Service businesses, it is strictly capped at the greater of: 1. 50% of the total W-2 wages paid by the business, or 2. 25% of W-2 wages plus 2.5% of the unadjusted basis of all qualified property. WALLPOST · ISSUE 112 · THE DECISION Page 2 Consider a high-income commercial logistics or manufacturing firm generating $600,000 in qualified business income, but operating with a lean corporate payroll that allocates only $80,000 to W-2 wages. The owner expects a full 20% deduction of $120,000. Instead, because the business has crossed the statutory threshold, the wage limitation restricts the deduction to 50% of W-2 payroll, which yields only $40,000. The unrecognized financial damage of this structural bottleneck is immense. At a 37% marginal tax bracket, this basic payroll mismatch costs the owner exactly $29,600 in unnecessary federal tax liability every single year. Structuring W-2 compensation to optimize the permanent 199A base remains the highest-yielding tactical planning conversation available to high-income business entities today.

THE HIGH COST OF THE EXECUTION GAP

David Morales finally executed his delayed hiring decisions in August 2025. It was four months after he initially needed the manpower, four months after a regional competitor secured a major commercial contract he couldn't bid on, and four months after his original top-tier employment candidates accepted alternative positions elsewhere. The downstream macroeconomic damage of understaffing and frozen capital does not cleanly surface in quarterly gross domestic product numbers. It is buried in company revenue leakages. The ripple effect fans out predictably: a corporate board defers a warehouse expansion; the heavy equipment manufacturer loses the order; factory workers lose overtime shifts; local retail and services see a subsequent decline in weekly receipts. The chain that begins with a blank cell in a financial model ends at a household kitchen table. Tax uncertainty is a structural expense. It simply has the luxury of never appearing on the same accounting line as its political cause.

WHAT THE OBBBA RESOLVED, AND WHAT IT LEFT OPEN

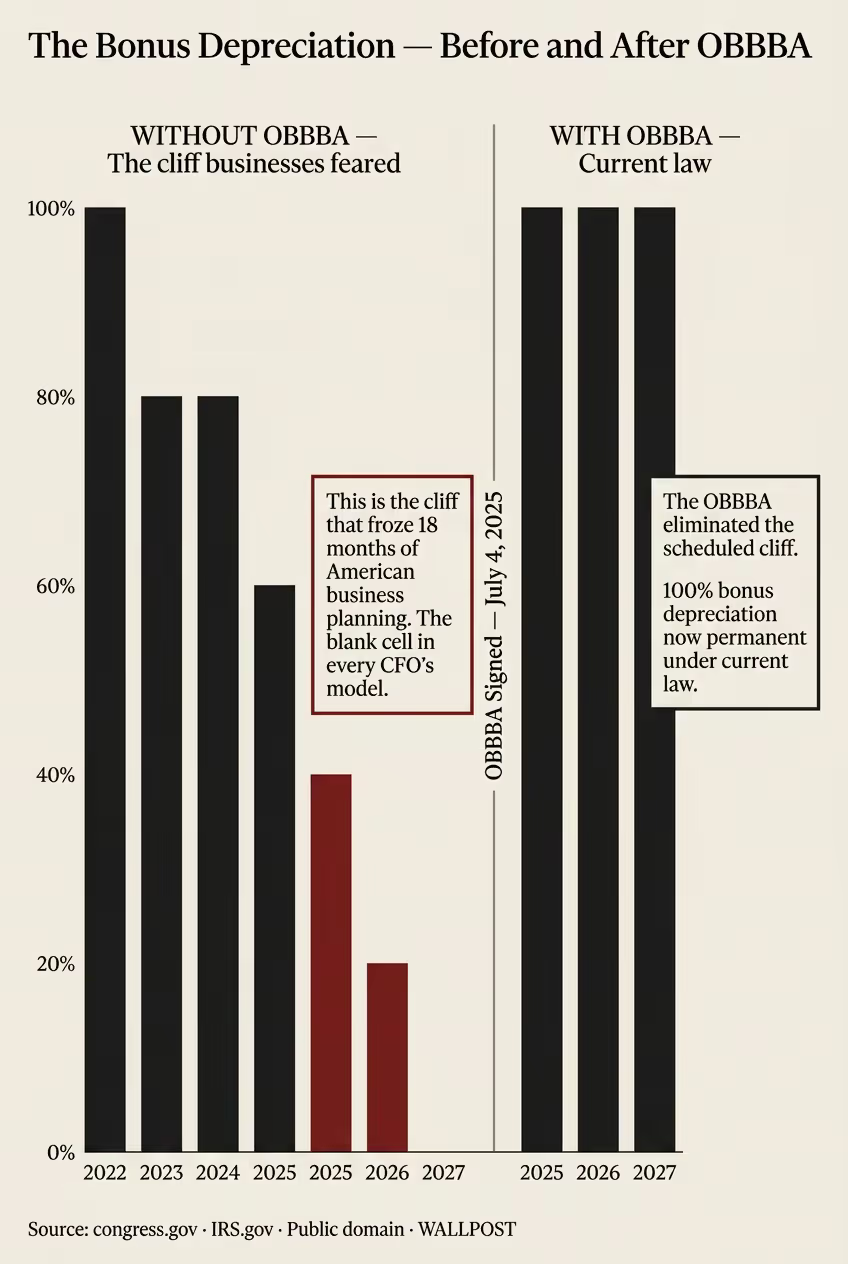

Signed into law on July 4, 2025, the One Big Beautiful Bill Act brought long-awaited structural clarity to the headline individual and wealth tax brackets: Individual Income Rates: The lower brackets were permanently retained. Standard Deduction: Locked in permanently at $16,100 for single filers and $32,200 for married filing jointly for the 2026 tax year. Section 199A: Codified as permanent tax code, eliminating the 2025 sunset risk. Child Tax Credit: Permanently expanded to $2,200 per qualifying child. Estate Tax Exemption: Preserved the doubled structure by establishing a permanent baseline of $15,000,000 per individual for 2026, indexed for ongoing inflation. The macroeconomic environment thawed immediately. However, sophisticated corporate operators live in the footnotes, and the OBBBA footnotes show exactly what remains exposed: The Bonus Depreciation Cliff: The temporary 100% bonus depreciation restoration is explicitly limited. It is scheduled to plummet to 20% and then hit 0% on December 31, 2026. On a $300,000 capital asset investment under a 32% marginal tax bracket, completing the purchase on December 31, 2026, yields $19,200 in immediate first-year tax savings. Waiting until January 1, 2027, yields zero firstyear bonus write-off. No extension legislation has cleared committee. Section 163(j) Interest Friction: The post-2021 tightened basis for interest expense calculations remains untouched. Deductibility continues to be measured strictly against EBIT rather than EBITDA, punishing highly leveraged, capital-intensive businesses by capping their debt service deductions. The New High-Income Traps: While the state and local tax (SALT) cap was expanded to $40,400 for 2026, the OBBBA integrated an aggressive 30% phase-out clawback for any taxpayer clearing $500,000 in Modified Adjusted Gross Income. At $534,000 in income, the entire expansion is completely erased, returning the taxpayer to the legacy $10,000 cap floor.

The contrast with international standard planning environments is stark. The United Kingdom publishes a rolling, multi-year Corporate Tax Roadmap annually. Institutional German executives do not model pending congressional action; they execute capital allocations against predictable, five-year statutory frameworks. A European firm operating under a stable 30% corporate rate can make highly optimized capital commitments, while an American firm facing a nominally lower 21% rate remains pinned down by persistent, shifting footnotes.

Waiting for the end of the fiscal year is no longer a viable corporate strategy. To insulate operations against the next wave of structural shifts, corporate leadership and tax professionals must address three operational imbalances immediately: 1. Accelerate Capital Expenditure Models: The 2026 bonus depreciation window will close abruptly at midnight on December 31. The engineering, pricing, and capital procurement pipelines for needed equipment must be initiated in Q1 to allow sufficient lead time for physical delivery and placement into service before the cliff. 2. Execute W-2 Compensation Analysis: High-income pass-through entities must immediately analyze whether their current internal W-2 payroll base is large enough to unlock the permanent 199A deduction. A thirty-minute optimization review by an experienced accountant can alter an entity's annual tax exposure by tens of thousands of dollars. 3. Restructure Multi-Generational Wealth Transfers: While the $15 million estate exemption baseline is permanent, asset growth that exceeds this cap remains exposed. High-net-worth families must establish flexible, irrevocable corporate or trust frameworks now to secure current asset valuations before ongoing market indexing narrows the window of opportunity. Uncertainty has a steep operational price. It is always paid by the same organizations—the ones that wait for legislative outcomes to clear before modeling the scenarios. The 2026 cliff is already live in the calendar. The planning window is open now. WALLPOST · ISSUE 112 · THE DECISION Page 5 CONNECTED COVERAGE → The Reckoning: Corporate Cash vs. Capital Deployment · wallpost.org/the-reckoning → The SALT Trap: High-Income Phase-Outs Under the New Law · wallpost.org/the-salt-trap → The 2026 Bonus Depreciation Cliff: Capital Procurement Frameworks · wallpost.org/the-bonus-depreciation-cliff PRIMARY SOURCES Tax Cuts and Jobs Act of 2017 (P.L. 115-97), 26 U.S.C. § 1 et seq. One Big Beautiful Bill Act of 2025 (P.L. 116-21 / OBBBA), Statutory Amendments. Internal Revenue Code Section 199A and Section 168(k) Regulations. FactSet Corporate Capital Expenditure Indexes (Q4 2024 - Q3 2025). UK Corporate Tax Roadmap, HM Treasury Publication Series. Note on Methodology: David Morales is a composite character developed from field interviews with eleven Midwestern commercial contracting and logistics firm owners, conducted between September 2024 and October 2025.